Investing Part 1

Lesson 12

Invest Today & Invest More

I know I over complicate the idea of saving and investing for goals. Since retirement should be on all our goal lists, I will focus on just that goal. But you can save and invest for small term goals like that Hawaiian trip you always wanted.

In the LDS Personal Finance Course Book there is a great illustration about investing. I just want to rephrase things so you can compare more simply.

JULIA

Invests $300/m from 25-65 years.

In total invests $147,600.

Doubles her money 5.8 times.

ANDREA

Invest 2x more monthly than Julia from 35-65 years.

In total invests 1 and a half times as much of what Julia did.

Doubles her money 3 times.

BELLA

Invest 4x more monthly than Julia from 45-65 years.

In total invests double what Julia did.

Doubles her money 1.4 times.

Do you see how you can’t make up for years of not investing? You need time consistently investing and on average a good return. Most people talk about compound interest. To me that really does not exist in investing but rather the idea that money put in smart places can be like a snowball picking up speed and growing as it falls down hill. Basically it is the opposite of the debt snowball growing your wealth instead of enslaving you to it. Take Julia, she nearly doubled her money 6 times over. The lesson is invest now, and never stop and increase the investment amount to hit your retirement goal which we will cover soon.

Definitions and Examples

You need to understand some terms to keep more of your investments growth and pay less in taxes. And contrary to some popular beliefs these are my definitions and understandings.

Investing

Investing expects an annualized (average return/years of investing) return higher than inflation and over the span of years. You can also look at risk and what past performance has been to try and inform your prediction of growth in the future.

I like the example of risk vs return in the book however you need to add a line for inflation. Something like this.

Inflation

Inflation exists and eats your money's buying power yearly regardless of what you do with that money. In general we understand it right now as a percentage like 2-3% inflation yearly. But in reality some things like buying luxuries, homes and food can vary wildly year to year. And in history we have had higher inflation and crumbling economies end up with astronomical inflation rates compared to the global market (another great reason for emergency fund, food storage and being out of consumer debt).

It should go without saying but you should try and get a higher return than inflation. And in general if an investment claims to get more than the stock markets average 8-12%(Not adjusted for inflation) then you should be very cautious.

Struggle to keep up with inflation (Bad places for investments):

- High yield savings account (this is a good place for emergency funds but not investments)

- CD

- Savings account

- Checking account

Barely keep up with inflation:

- Bonds (Preferably USA Treasury bonds)

Passive Investments

Passive investments are the only way to keep earning money even if you can no longer contribute money (Lose job, get injured, die…). Everyone should be invested in passive investments and have 50% or more of their investments allocated to them. Stock and bond investments are passive.

The best balance between return and low risk seems to be in index or whole market funds. These stock or bond funds try to recreate the growth of the whole market so you can ride on average the return of that asset class. Individual stocks are way too much like gambeling. Watchout for index funds that are weighted to highly in one industry. For example most SNP 500 index funds are heavily weighted on the technology industry like 30% overweight. Means if that industry takes a hit you get hit too hard.

So look for USA and global whole market funds or equal weighted market funds.

Active Investments

Are often more risky but not always. The risk increases with little proven years of track record and the more actively involved you have to be. If you are young you can afford more risk and have a longer time to recover from a blunder. For instance starting a side hustle, going to college to obtain better employment or starting a business or investing in businesses are all risky. But the returns can be great. So you have to limit this to say 50% or less of your overall investment plan.

Alternative Investments

There is a broad category the rich are using to grow their annual wealth by an average of 5%. They call it “Alternatives”. I’m having a hard time finding average returns and examples in these more active investments. However there are some stock and stock indexes for some of these types of investments.

Alternative Investments Examples:

- Business ownership (My favorite)

- Real Estate (Private, group owned/managed, development, land)

- Private Capital (investing in businesses, secured loans)

- Venture Capital

- Timber

- Buyout

- Private equity

- Hedge funds (something I will never do)

- Gold and silver (something I will never do)

- ...

Investments I Will Not Touch

These are the investments I will never touch.

Speculations

Value only increases based on perception of future buyers. At least stocks are part ownership in a real company and can be compared between other companies Price to Earnings ratios.

These are some of the common speculations: Bitcoin (not sure this is ethical either), gold and silver, antiques and collectibles.

Gambeling

Anything labeled gambling or picking individual stocks.

Other

Not sure where these fall but I will never touch them.

Day trading, private loans, unsecured loans, annuities (not an investment but rather insurance).

Investment Mindset

The number one thing that will sink investment success is your human mindset pitfalls. Pitfalls like not investing, or trying to time the market (Avoid all risk to try and get a reward). The next worst is not having enough time for long term investments to pan out. Under investing is also a problem. And of course to picking to risky investments and having no diversification sink peoples investment returns.

This video is more than just investing, it covers many of the human emotions and pitfalls around money. I really like the idea of when the market is down this is not a fee or punishment for doing something wrong, it's an admission fee for long term gains.

Here is my summary of the Phycology of Money - very good at helping you get over your mental blocks and start investing.

Dave Ramsey is also very good in his trainings and books at talking about the emotional pitfalls most people fall into.

Picking a Goal For Retirement

“If you fail to plan now, you may not have enough income or savings to be self-reliant after you retire.” Invest For The Future Part 2

Now you understand some basic asset classes and how inflation steals your money's buying power. Now you need to set a goal for the date of your retirement and how much money you will want when you get there.

For that I turn to the Guru David Stein who runs the podcast Money For The Rest of Us.

For my wife and I we need to get to the point we are putting $1k away per month towards investments to hit our goal of 1 Million or more by the time we retire. Note I put the return as a modest 6%.

Here is the Money For the Rest of Us version of a Retirement Planning calculator/spreadsheet.

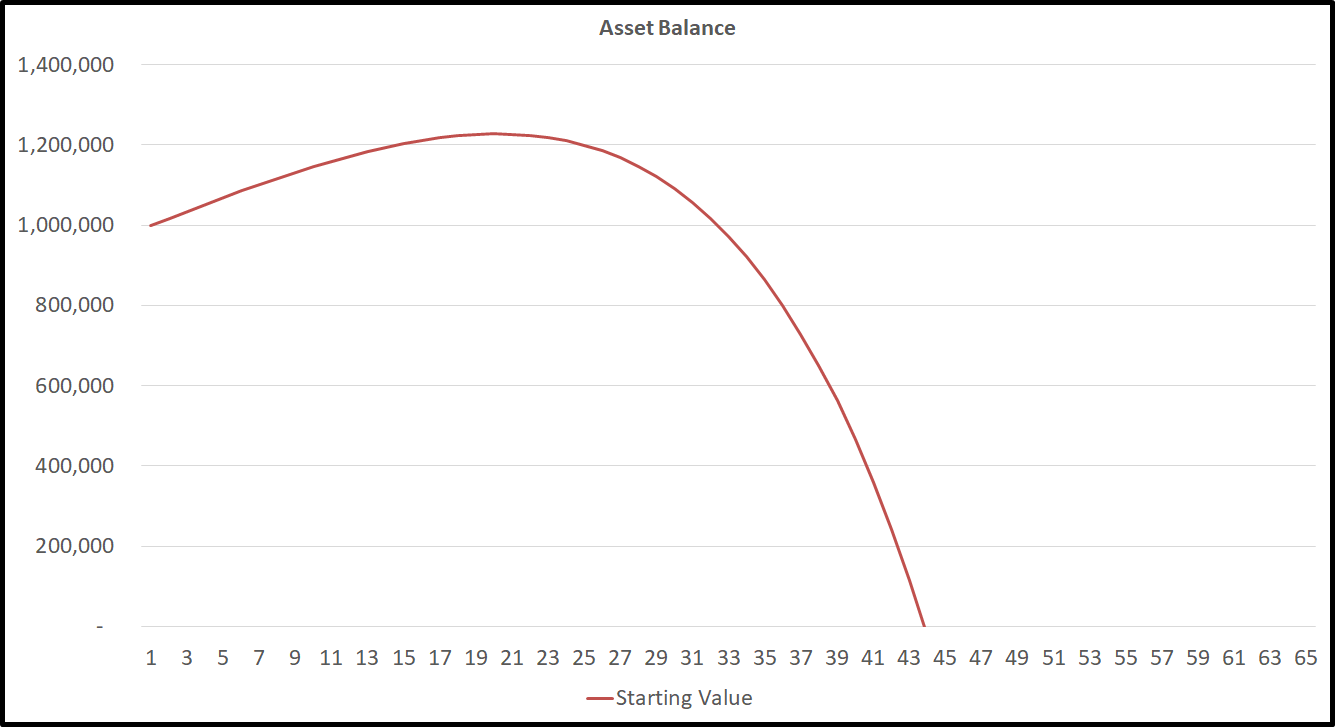

And in his example you can use the rule of thumb many use of trying to only spend 4% annually of your investment total (nest egg). Remember by the time you retire you should have your home paid off and this just $40k to live and have fun on yearly.

Version of a Retirement Spending calculator/spreadsheet mentioned in Episode 244, 243 and 161.

This example goes well past the 20-30 years most people will live after they retire at 65.

Please note that when your investments take a dressing hit, even in retirement, you may have to take less thank 4% for many years to avoids running out of money before you die. You may also need to go back to work or work a side hustle for a time. Because of this fear many, choose to have little in stock or other investments by the time they retire but they also miss out on returns. Many choose to maintain 30-40% of their investments in stock during retirement as a more on conservative middle ground.

The retirement spending spreadsheet is the same as Mind the Gap spreadsheet and video I mentioned in Episodes 149, 119 and 33.

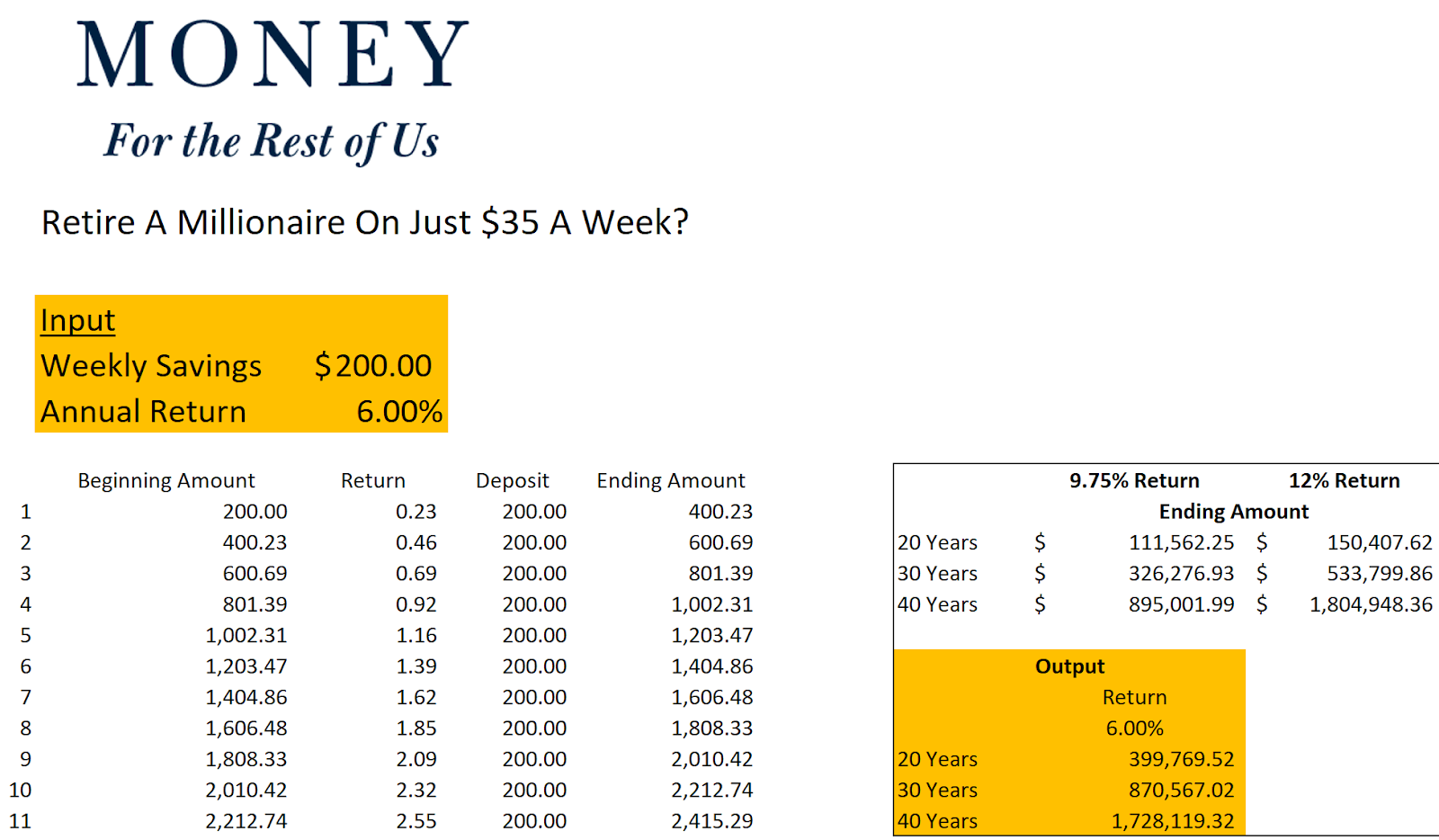

Here is the link to the Can You Become A Millionaire Saving $35 a Week and here is the link to Am I Saving Enough To Retire spreadsheet and video, mentioned in Episode 138 and Episode 129.

Here is the link to the Am I Saving Enough To Retire Early Spreadsheet from Episode 13.

The FIRE community says you can retire (really be happy and keep working how you want) when you have saved up and invested 10x your annual income. I think that is a rather low number and you will be hurting in retirement unless you can supplement that with a job or a side business. Some also believe that when your income from investments (Passive investments) monthly is higher than your expenses, you have hit financial freedom (the crossover point).

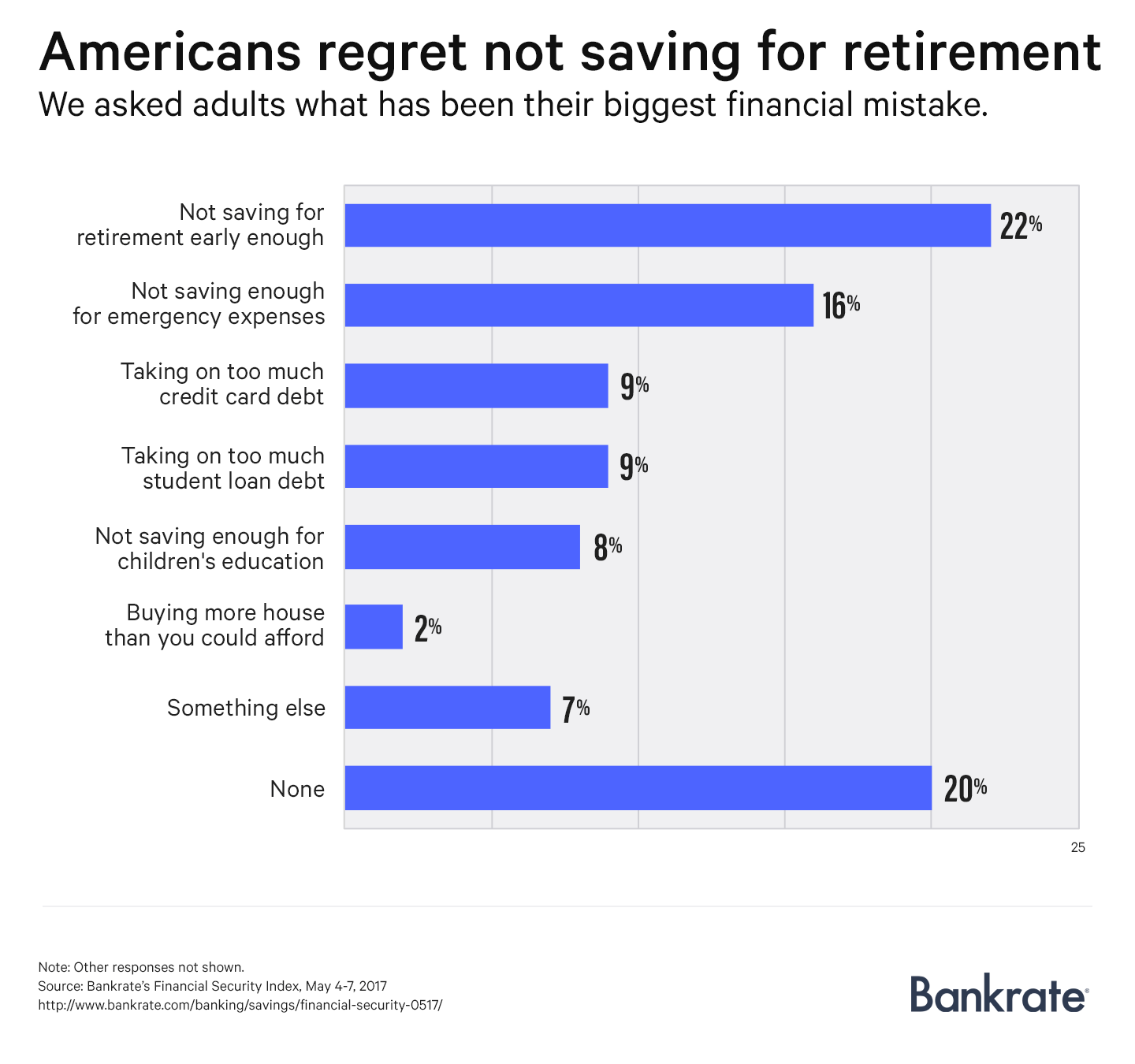

Regrets

Only 20% of Americans have no regrets about saving for retirement. So make sure you aren’t one of the 80% left wanting.

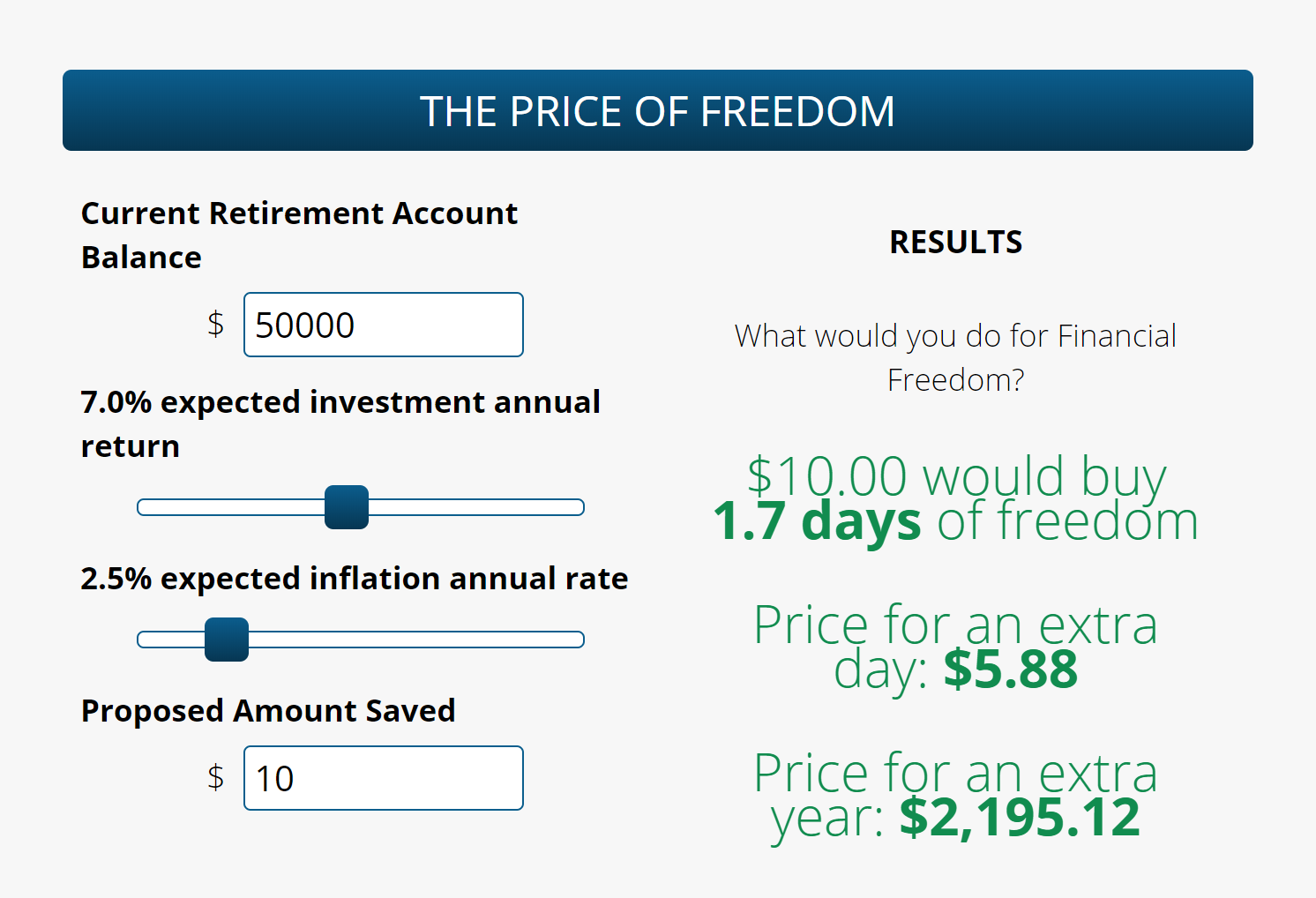

Freedom Calculator

There once was a interesting calculator that calculated how much freedom and time are you trading for it your comfort now. This calculation is an amazing idea and shows how much even an extra 2k invested in a year could mean as much as retiring a whole year sooner. I’m not sure how it works but I have to say it is rather motivational when it comes to saving a little more yearly.